In this blog, Jeremy Bliss, a Business Development Director with Icon Solutions, discusses why there is no room for manoeuvre with the 2019 deadline for the Hungarian instant payments scheme.

An important meeting took place this week in Budapest between the Hungarian National Bank (MNB); Giro Zrt, who will operate the country’s new instant payment scheme; and Nets who will build it; plus the various financial institutions that will connect to it. All of them gathered to discuss progress with the Hungarian instant payments project. The feedback was clear – the July 2019 launch date of Hungary’s national instant payments scheme is not moving.

To demonstrate just how serious they are about this deadline, MNB will be issuing a compulsory monthly questionnaire to all Hungarian banks to assess their readiness for instant payments. If the answers aren’t satisfactory, the issue will be escalated to the bank’s senior management. MNB has a clear vision for instant payments in Hungary and there is no leeway for banks wanting to postpone the deadline.

Banks cannot avoid taking action

From our conversations with Hungarian banks it is clear that some have started planning for their instant payments implementation projects, but there is still a large number of banks who have not yet formed a strategy to tender or established a clear path to go live in July 2019. With the pressure on meeting the deadline so high, why are some banks hesitating in their plans? The absence of the Technical Connectivity and Scheme Technical Specifications from Giro and Nets is clearly one factor, but that alone should not hinder plans for instant payments in Hungary.

In our view, banks in Hungary should be leveraging the SCT Inst rulebook published by the European Payments Council to help guide them on the requirements for technology solutions for instant payments. The Hungarian domestic instant payments scheme is shaped closely on the SCT Inst rulebook – so, although there will be some local nuances – it is safe to say that this gives a very clear idea of what the specifications for Hungary will eventually include. This rulebook provides banks with the important information they need on the expected functional flows, high level messaging formats and data requirements of the Hungarian domestic scheme. And this in turn enables them to start identifying the types of technology solutions for their instant payments service.

A mandated timeline alone should not be the sole driver behind the adoption of instant payments. Early adopters of the scheme will be perceived as modern and millennial focused – they will be able to deliver innovative new products and services to their customers and be able to extend their digital services via APIs. Not only that, but as a result of instant payments, banks can improve their cash-flow management and increase their e2e payments process automation. They will also benefit from the cost reduction in managing cash and cheques, savings that can be reinvested in their product development strategy.

Where next – identifying the technology solution

The focus at the moment is of course on meeting the July 2019 deadline and finding a solution that can support the high volumes and straight-through processing requirements of instant payments. However, it is also important that banks in Hungary select technology solutions that provide them with long term advantages to help protect their payments business from market disruptors such as Amazon, Apple and Google. Innovation will be key to keeping ahead of the competition and their solution for instant payments needs to be flexible enough to adapt to the demands of tomorrow.

From our experience working with other instant payments schemes, such as the UK’s Faster Payments or Singapore’s FAST, a flexible open source approach enables banks to meet the needs of the short and long term. Icon’s IPF product has not only been designed specifically for instant payments, but it is also based on a forward-looking technology stack that meets the requirements of the API economy and encourages the adoption of open source technologies, DevOps and subsequent full agile development. This new solution will allow banks to offer innovative payment services without affecting the existing payment services built on batch systems.

Working to a clear timeline

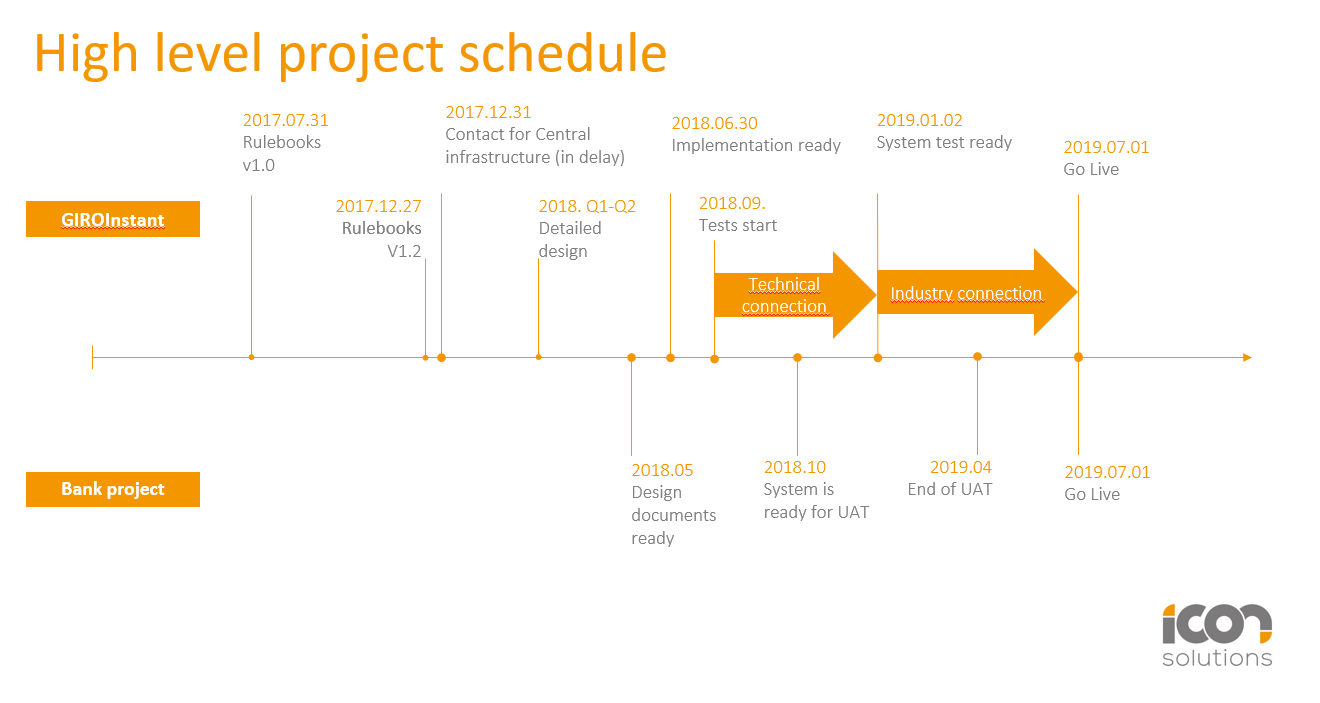

In Hungary the path to domestic instant payments will be two years from conception to launch. This will be an incredible achievement for the market (by comparison, the Dutch instant payment scheme took several years) but it also means that many milestones need to be delivered within a compressed timeline.

Below is our view on the key tasks that will need to be achieved between now and the 1st July next year.

Our work on a number of RFIs/RFP’s for Hungarian banks means that we are very close to the specific challenges and requirements of the Hungarian instant payments scheme. Hungarian banks must make some crucial decisions around the selection of instant payments processing solutions to not only fit their organisation’s business and IT requirements today but for the needs of tomorrow. It is important that they avoid the long and drawn out complex journey of ‘ripping & replacing’ their existing systems and instead focus on complementing their existing payments platform with a modern, open source based and API friendly dedicated solution. This will not only address the instant payments needs but it will also provide flexibility to quickly launch new payment products in future.

Icon’s IPF is one such solution that can address these requirements. We are already working with a number of Hungarian banks on their instant payments projects and look forward to enabling our customers to face the challenges and opportunities of the future head-on.